1. Introduction

Financial Industry Regulatory Authority (“FINRA”) supervisory control rules1See FINRA Rule 3110 (Supervision). require each securities broker-dealer that is a member of FINRA to categorize every location from which the business of the broker-dealer is regularly conducted as either (a) a branch office, (b) an “office supervisory jurisdiction” (“OSJ”), which is an office from which certain supervisory activities occur, or (c) a non-branch location.2See FINRA Rule 3110(a)(3) and (f). Appropriate supervision and control is required to be maintained over all such locations, with the supervisory obligations varying based in part on the office category of the location. For example, branch offices and OSJs are expected to be subject to office inspection at least annually. For non-branch locations, inspections are required not less frequently than once every three years.

Under current rules, a personal residence from which broker-dealer associated persons work on a regular basis can be deemed to be a “non-branch location”, provided that various requirements are met.3See FINRA Rule 3110(f)(2)(ii). This residential office exception, however, does not apply to an office that would otherwise be categorized as an OSJ due to the activities taking place there.

During the COVID pandemic, FINRA issued special relief that facilitated broker-dealer activities taking place from a residential location, including with respect to office categorization, and also with respect to remote inspections of residential offices.4See FINRA Regulatory Notice 20-08, “Pandemic-Related Business Continuity Planning, Guidance and Regulatory Relief” (March 9, 2020). See also Rule 3110.17 (“Temporary Relief to Allow Remote Inspections for Calendar Years 2020, 2021, 2022, 2023, and Through the Earlier of the Effective Date of the Remote Inspections Pilot Program, if Approved, or June 30, 2024.”), (Together, the “2020 Regulatory Relief”)

In 2022, FINRA, proposed to modify its supervisory control rules to permit both (a), remote office inspections5See SEC Release 34-96520, “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Notice of Partial Amendment No. 1 to Proposed Rule Change to Adopt Supplementary Material .18 (Remote Inspections Pilot Program) under FINRA Rule 3110 (Supervision)” (December 16, 2022), withdrawn and replaced by SR-FINRA-2023-06. by member broker dealers, and (b) the establishment of a new category, “residential supervisory location” (“RSL”), which would permit certain supervisory activities to occur from a residential office without that office being deemed to be an OSJ6See SEC Release 34-96191, “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Order Instituting Proceedings to Determine Whether to Approve or Disapprove a Proposed Rule Change to Adopt Supplementary Material .19 (Residential Supervisory Location) (October 31, 2022), withdrawn and replaced by SR-FINRA-2023-07.. RSLs are instead treated as non-branch locations for purposes of the supervisory control rules. These proposals were withdrawn and refiled in 2023.7See SEC Release 34-97398, “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Notice of Filing of a Proposed Rule Change to Adopt Supplementary Material .18 (Remote Inspections Pilot Program) under FINRA Rule 3110 (Supervision)” (April 28, 2023) (“Remote Inspections Proposing Release”). See also, SEC Release 34-96191, “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Notice of Filing of a Proposed Rule Change to Adopt Supplementary Material .19 (Residential Supervisory Location) under FINRA Rule 3110 (Supervision)” (March 31, 2023) (“RSL Proposing Release”).

On November 17, 2023, the U.S. Securities and Exchange Commission (“SEC”) adopted these FINRA proposals.8See SEC Release 34-98982 “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Order Approving a Proposed Rule Change to Adopt Supplementary Material .18 (Remote Inspections Pilot Program) under FINRA Rule 3110 (Supervision)”, (November 17, 2023) (“Remote Inspection Adopting Release”), and see also SEC Release 34-98980, “Self-Regulatory Organizations; Financial Industry Regulatory Authority, Inc.; Notice of Filing of Amendment No. 2 and Order Granting Accelerated Approval of a Proposed Rule Change, as Modified by Amendment Nos. 1 and 2, to Adopt Supplementary Material .19 (Residential Supervisory Location) under FINRA Rule 3110 (Supervision)”, November 17, 2023 (“Residential Supervisory Location Adopting Release”). The Remote Inspection Adopting Release was published in the Federal Register on November 24, 2023: see 88 Fed. Reg. 82464 (November 24, 2023). The Residential Supervisory Location Adopting Release was published in the Federal Register on that same day: see 88 Fed. Reg. 82447 (November 24, 2023).

Following the effective date of the new rules, FINRA, members will be able to categorize locations from which the business of the broker dealers conducted in one of four categories (branch office, OSJ, RSL, and non-branch location), rather than the previous three categories. Broker-dealers will also be able to conduct remote office inspections.

The new rules are subject to a host of conditions and exclusions, and both the designation of a location as an RSL, and the remote inspection of offices must be subject to written supervisory procedures that are reasonably designed to achieve compliance with the applicable conditions.

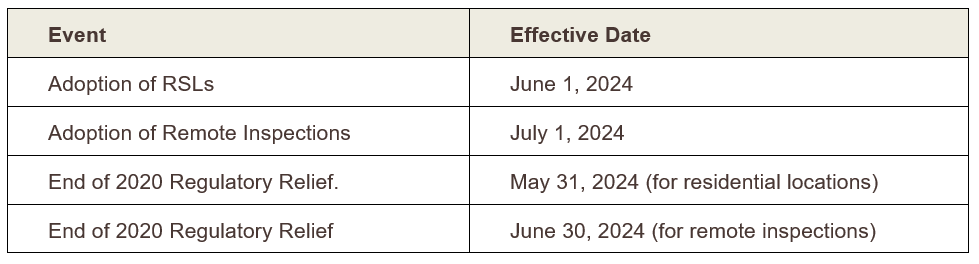

In January 2024, FINRA issued Regulatory Notice 24-02 announcing adoption of these proposals, and noting the following effective dates:

The remainder of this note describes the new rules in detail.

2. Residential Supervisory Locations

a. What is a Residential Supervisory Location?

As noted above, a RSL is a new category of broker-dealer office location, supplementing the existing three categories found in FINRA Rule 3110: non-branch locations, branch offices, and OSJs. A RSL is a location that is the associated person’s private residence, where supervisory activities are conducted, including those described in Rule 3110(f)(1)(D) through (G) or in Rule 3110(f)(2)(B)9The activities specifically enumerated as supervisory activities for purposes of the RSL designation are: “(D) final acceptance (approval) of new accounts on behalf of the member; (E) review and endorsement of customer orders; (F) final approval of retail communications for use by persons associated with the member, pursuant to Rule 2210(b)(1), except for an office that solely conducts final approval of research reports; or (G) responsibility for supervising the activities of persons associated with the member at one or more other branch offices of the member.” Also enumerated is the activity described at Rule 3110(f)(2)(B): “any location that is responsible for supervising the activities of persons associated with the member at one or more non-branch locations of the member […].” Notably absent from the definition of RSL are the activities described by Rule 3110(f)(2)(A) through (C): “(A) order execution or market making; (B) structuring of public offerings or private placements; (C) maintaining custody of customers’ funds or securities […]”. The RSL Proposing Release notes – and confirms – the absence of these activities, and concludes as follows: “Longer term, FINRA expects to reassess the OSJ and branch office definitions under Rule 3110(f) more generally as part of its continued efforts to modernize FINRA rules.” Firms that will be permitting personnel to conduct such excluded activities from residential locations must now treat such locations as OSJs; note also that some firms will need to consider whether an application for expansion is required with FINRA in order to accommodate remote work from excluded locations.. A RSL will be considered for those activities to be a non-branch location, provided that the other restrictions and limitations described below are met.

b. Conditions for designation as a Residential Supervisory Location

In order to designate a residential location as a RSL, the location must meet the following conditions:

- only one associated person, or multiple associated persons who reside at that location and are members of the same immediate family, conduct business at the location;

- the location is not held out to the public as an office;

- the associated person does not meet (in person) with customers or prospective customers at the location;

- any sales activity that takes place at the location complies with the conditions set forth under Rule 3110(f)(2)(A)(ii) or (iii)10The conditions found under Rule 3110(f)(2)(A)(ii) and (iii) are largely redundant to the RSL location restrictions. The non-redundant requirements are: “(ii) […] g. All orders are entered through the designated branch office or an electronic system established by the member that is reviewable at the branch office; h. Written supervisory procedures pertaining to supervision of sales activities conducted at the residence are maintained by the member; and i. A list of the residence locations is maintained by the member; and, (iii) Any location, other than a primary residence, that is used for securities business for less than 30 business days in any one calendar year […]”;

- neither customer funds nor securities are handled at that location;

- the associated person is assigned to a designated branch office, and such designated branch office is reflected on all business cards, stationery, retail communications and other communications to the public by such associated person;

- the associated person’s correspondence and communications with the public are subject to the firm’s supervision in accordance with this Rule;

- the associated person’s electronic communications (e.g., e-mail) are made through the member’s electronic system;

- (A) the member must have a recordkeeping system to make and keep current, and preserve records required to be made and kept current, and preserved under applicable securities laws and regulations, FINRA rules, and the member’s own written supervisory procedures under Rule 3110; (B) such records are not physically or electronically maintained and preserved at the office or location; and (C) the member has prompt access to such records; and

- the member must determine that its surveillance and technology tools are appropriate to supervise the types of risks presented by each Residential Supervisory Location, and these tools may include but are not limited to: (A) firm-wide tools such as, electronic recordkeeping system; electronic surveillance of e-mail and correspondence; electronic trade blotters; regular activity-based sampling reviews; and tools for visual inspections; (B) tools specific to the RSL based on the activities of associated person assigned to the location, products offered, restrictions on the activity of the RSL; and (C) system tools such as secure network connections and effective cybersecurity protocols.

c. Member ineligibility criteria

In order for a FINRA member to designate associated persons’ locations as RSLs, that broker-dealer must not be ineligible. A broker-dealer will be ineligible to designate an office or location as an RSL if the member:

- is currently designated as a Restricted Firm under Rule 4111;

- is currently designated as a Taping Firm under Rule 3170;

- is currently undergoing, or is required to undergo, a review under Rule 1017(a)(7) as a result of one or more associated persons at such location;

- receives a notice from FINRA pursuant to Rule 9557 (Procedures for Regulating Activities under Rule 4110 (Capital Compliance), Rule 4120 (Regulatory Notification and Business Curtailment) or Rule 4130 (Regulation of Activities of Section 15C Members Experiencing Financial and/or Operational Difficulties)), unless FINRA has otherwise permitted activities in writing pursuant to such rule;

- is or becomes suspended by FINRA;

- based on the date in the Central Registration Depository (CRD), had its FINRA membership become effective within the prior 12 months; or

- is or has been found within the past three years by the SEC or FINRA to have violated Rule 3110(c)11Rule 3110(c) is the portion of FINRA Rule 3110 that requires each FINRA member broker-dealer to conduct an annual assessment of its compliance function. The member ineligibility criteria establish an important new collateral consequence for firms to consider when negotiating enforcement matters with FINRA..

d. Location ineligibility criteria

An office or location will not be eligible for designation as an RSL if one or more associated persons at such office or location:

- is a designated supervisor who has less than one year of direct supervisory experience with the member, or an affiliate or subsidiary of the member that is registered as a broker-dealer or investment adviser;

- is functioning as a principal for a limited period (in accordance with FINRA Rules);

- is subject to a mandatory heightened supervisory plan under the rules of the SEC, FINRA or state regulatory agency;

- is statutorily disqualified, unless such disqualified person has been approved (or is otherwise permitted pursuant to FINRA rules and the federal securities laws) to associate with a member and is not subject to a mandatory heightened supervisory plan as a condition to approval or permission for such association;

- has an event in the prior three years that required a “yes” response to any item in Questions 14A(1)(a) and 2(a), 14B(1)(a) and 2(a), 14C, 14D and 14E on Form U4;12Form U4 is the Uniform Application for Securities Industry Registration or Transfer for individuals. The relevant questions cited are: “14A(1) Have you ever: (a) been convicted of or pled guilty or nolo contendere (“no contest”) in a domestic, foreign, or military court to any felony? (2)(a) Based upon activities that occurred while you exercised control over it, has an organization ever: been convicted of or pled guilty or nolo contendere (“no contest”) in a domestic or foreign court to any felony? 14B(1) Have you ever: (a) been convicted of or pled guilty or nolo contendere (“no contest”) in a domestic, foreign or military court to a misdemeanor involving: investments or an investment-related business or any fraud, false statements or omissions, wrongful taking of property, bribery, perjury, forgery, counterfeiting, extortion, or a conspiracy to commit any of these offenses? (2)(a) Based upon activities that occurred while you exercised control over it, has an organization ever: been convicted of or pled guilty or nolo contendere (“no contest”) in a domestic or foreign court to a misdemeanor specified in 14B(1)(a)?” Question 14C outlines a broad array of findings made by the SEC or CFTC. Question 14D outlines a broad array of findings made by any other Federal regulatory agency or any state regulatory agency or foreign financial regulatory authority. 14E outlines a broad array of findings made by FINRA or other self-regulatory organizations. or

- has been notified in writing that such associated person is now subject to, any Investigation or Proceeding by the SEC, FINRA or another self-regulatory organization, or state securities commission (or agency or office performing like functions) (each, a “Regulator”) expressly alleging they have failed reasonably to supervise another person subject to their supervision, with a view to preventing the violation of any provision of the Securities Act, the Exchange Act, the Investment Advisers Act, the Investment Company Act, the Commodity Exchange Act, any state law pertaining to the regulation of securities or any rule or regulation under any of such Acts or laws, or any of the rules of the MSRB or other self-regulatory organization, including FINRA.13Note, however, that under the newly adopted Rule, such office or location may be designated or redesignated as an RSL subject to the requirements of this Supplementary Material upon the earlier of: (i) the member’s receipt of written notification from the applicable Regulator that such Investigation has concluded without further action; or (ii) one year from the date of the last communication from such Regulator relating to such Investigation.

e. Procedural obligations: risk assessment and list of RSLs

A broker-dealer that designates residential locations as RSLs has important procedural obligations. The first is to make a risk assessment prior to designating a RSL, and the second is to provide a list of RSLs to FINRA.

1. Requirement to make a risk assessment prior to designating a RSL

Prior to designating an office or location as an RSL, FINRA-member broker-dealers must develop a reasonable, risk-based approach to designating such office or location as an RSL. The FINRA member must both (a) conduct and (b) document a risk assessment for the associated person assigned to that office or location.

The assessment must document the factors considered, including among others, whether the associated person at such office or location is now subject to: (1) customer complaints, taking into account the volume and nature of the complaints; (2) heightened supervision other than where such office or location is ineligible for RSL designation; (3) any failure to comply with the member’s written supervisory procedures; (4) any recordkeeping violation; and (5) any regulatory communications from a Regulator, indicating that the associated person at such office or location failed reasonably to supervise another person subject to their supervision.

As part of this risk assessment, the broker-dealer must take into account any higher-risk activities that take place or a higher-risk associated person that is assigned to that office or location. Generally, the firm must take into consideration any red flags relating to irregularities or misconduct in determining whether it is reasonable to maintain the RSL designation of such location.

2. Requirement to produce a list of RSLs to FINRA

A member that elects to designate any office or location of the member as an RSL must provide FINRA with a current list of all locations designated as RSLs by the 15th day of the month following each calendar quarter in the manner and format (e.g., through an electronic process or such other process) as FINRA may prescribe. The first RSL list is due to FINRA on October 15, 2024, covering all locations firms designate as RSLs during the period June 1, 2024, through September 30, 2024.14See Regulatory Notice 24-02. FINRA states in that Notice that it is currently developing a technological process in FINRA Gateway through which firms will be able to identify their RSLs and meet the obligation to provide their quarterly RSL lists to FINRA in an efficient manner. FINRA expects such technological process to be ready no later than May 31, 2024. FINRA states that they expect to publish additional guidance detailing the operational process for the submission of the quarterly RSL list to FINRA.

3. Remote Inspections

a. Pilot program

New Rule 3110.18 establishes a voluntary, three-year remote inspections pilot program (the “Pilot Program”) to allow eligible FINRA-member firms to fulfill their Rule 3110 inspection obligations of their locations, including branch offices, OSJs, non-branch locations – and now RSLs – remotely, without an on-site visit to such offices or locations. A firm must affirmatively elect to participate in the Pilot Program by providing FINRA with an “opt-in notice” and once enrolled, must affirmatively elect to withdraw from the Pilot Program by providing FINRA with an “opt-out notice,” in the form and manner prescribed by FINRA.15For Pilot Program Year 1, which starts on July 1, 2024, and ends on December 31, 2024, the timeframe in which an eligible firm may elect to opt in to the Pilot Program is June 1, 2024, through June 26, 2024. An eligible firm that does not elect to join Pilot Year 1 by June 26, 2024 may choose to join the Pilot Program for a subsequent Pilot Year on or before these December 27, 2024 (to join Pilot Year 2), December 27, 2025 (to join Pilot Year 3), and December 27, 2026 (to join Pilot Year 4, which lasts from January 1, 2027, to June 30, 2027). In general, a firm must withdraw from the Pilot Program by December 27 of any year in order to withdraw in the subsequent year. In Regulatory Notice 24-02, FINRA states that it is currently developing a technological process in FINRA Gateway through which firms will be able to provide FINRA the requisite notices electronically. FINRA states that it will provide further details about the manner and format of these notices in subsequent guidance.

b. Risk assessment requirement and factors to consider

Prior to electing a remote inspection for an office or location, rather than an on-site inspection, the FINRA-member firm must develop a risk-based approach to using remote inspections and conduct and document a risk assessment for that office or location.

The assessment must document the factors considered, including the factors set forth in Rule 3110.1216FINRA Rule 3110.12 sets standards for reasonable review of a firm’s businesses. The factors cross-referenced in the Remote Inspections rule are: “the firm’s size, organizational structure, scope of business activities, number and location of the firm’s offices, the nature and complexity of the products and services offered by the firm, the volume of business done, the number of associated persons assigned to a location, the disciplinary history of registered representatives or associated persons, and any indicators of irregularities or misconduct (i.e., “red flags”), etc.” In addition to the factors set out in Rule 3110.12, the Remote Inspections rule requires a firm to consider the following factors: (A) the volume and nature of customer complaints; (B) the volume and nature of outside business activities, particularly investment-related; (C) the volume and complexity of products offered; (D) the nature of the customer base, including vulnerable adult investors; (E) whether associated persons are subject to heightened supervision; (F) failures by associated persons to comply with the member’s written supervisory procedures; and (G) any recordkeeping violations. In addition, FINRA notes that firms should conduct on-site inspections or make more frequent use of unannounced, on-site inspections for high-risk offices or locations or where there are indicators of irregularities or misconduct (i.e., “red flags”). and must take into account any higher-risk activities that take place at, or higher-risk associated persons that are assigned to, that office or location.

A member or its office or location that is ineligible for remote inspections because of the criteria noted below must conduct an on-site inspection of that office or location.

c. Written supervisory procedures and documentation requirements

1. Written supervisory procedures requirement

Under the new Rule, a member that elects to participate in the Pilot Program must establish and maintain written supervisory procedures regarding remote inspections that are reasonably designed to achieve compliance with applicable securities laws and regulations. In the Rule, FINRA states that reasonably designed procedures for conducting remote inspections of offices or locations must address, among other things:

- the methodology, including technology, that may be used to conduct remote inspections;

- the factors considered in the risk assessment made for each applicable office or location;

- the applicable procedures themselves; and,

- the use of other risk-based systems employed generally by the member to identify and prioritize for review those areas that pose the greatest risk of compliance failures.

2. Documentation requirement

Firms that opt into the Pilot Program must retain specified books and records regarding remote inspections. Specifically, books and records must identify:

- all offices or locations that were inspected remotely; and

- any offices or locations for which the member determined to impose additional supervisory procedures or more frequent monitoring (and what such additional procedures were).

3. Firm-level ineligibility criteria

Firms are not eligible to conduct remote inspections of any offices or locations if any time during the Pilot Program the firm:

- is or becomes designated as Restricted Firm under Rule 4111;

- is or becomes designated as a Taping Firm under Rule 3170;

- receives a notice from FINRA pursuant to Rule 9557 regarding compliance with Rule 4110 (Capital Compliance), Rule 4120 (Regulatory Notification and Business Curtailment) or Rule 4130 (Regulation of Activities of Section 15C Members Experiencing Financial and/or Operational Difficulties);

- is or becomes suspended from membership by FINRA;

- based on the date in the Central Registration Depository (CRD), had its FINRA membership become effective within the prior 12 months; or

- is or has been found within the past three years by the SEC or FINRA to have violated Rule 3110(c) (Internal Inspections)17See footnote 11 above..

4. Location-level ineligibility criteria

An office or location is not eligible for a remote inspection if at any time during the Pilot Program:

- one or more associated persons at such office or location is or becomes subject to a mandatory heightened supervisory plan under the rules of the SEC, FINRA or a state regulatory agency;

- one or more associated persons at such office or location is or becomes statutorily disqualified, unless such disqualified person has been approved (or is otherwise permitted pursuant to FINRA rules and the federal securities laws) to associate with a member and is not subject to a mandatory heightened supervisory plan, or otherwise as a condition to approval or permission for such association;

- the firm is or becomes subject to Rule 1017(a)(7) as a result of one or more associated persons at such office or location;

- one or more associated persons at such office or location has an event in the prior three years that required a “yes” response to any item in Questions 14A(1)(a) and 2(a), 14B(1)(a) and 2(a), 14C, 14D and 14E on Form U4;18See footnote 12 above.

- one or more associated persons at such office or location is or becomes subject to a disciplinary action taken by the member that is or was reportable under Rule 4530(a)(2);19A notice must be made to FINRA under Rule 4530(a)(2) if “an associated person of the [FINRA] member is the subject of any disciplinary action taken by the member involving suspension, termination, the withholding of compensation or of any other remuneration in excess of $2,500, the imposition of fines in excess of $2,500 or is otherwise disciplined in any manner that would have a significant limitation on the individual’s activities on a temporary or permanent basis.”

- one or more associated persons at such office or location is engaged in proprietary trading, including the incidental crossing of customer orders, or the direct supervision of such activities; or

- the office or location handles customer funds or securities.

5. Data collection requirement

Any firm that participates in the Pilot Program must collect a wide swath of data and provide those data to FINRA on a quarterly basis. This data includes information regarding:

- The number of offices and locations with an inspection completed during each calendar quarter;

- The number of offices and locations that were inspected remotely;

- The number of offices and locations that were inspected on-site;

- The number of offices and locations that were inspected on-site because of a finding;

- The number of offices and locations where findings were identified, the number of those findings and a list of the significant findings; and

- Certain requirements of the written supervisory procedures for Remote Inspections.

4. Conclusion

The expansion of broker-dealers’ ability to permit flexible working arrangements through the introduction of the RSL category and through conduct of remote inspections is a welcome one. Not only are flexible working arrangements now the norm in the financial industry, but the ability to offer more flexible working arrangements better allows broker-dealers to attract and retain talent, especially talent from groups that are historically under-represented in the industry. Furthermore, various financial industry participants that compete with broker-dealers for talent can offer flexible working arrangements, and the absence of the RSL category would put broker-dealers at a disadvantage in seeking to hire and retain talent—especially talent from under-represented groups.

Broker-dealers must now turn their attentions to compliance with the many, many conditions and requirements in order to take advantage of these new rules, including the various procedures and assessments that are required prior to designating a RSL or conducting remote inspections.